How Interest Rates Impact Roll-Ups

Over the past fifteen years, the private equity industry relied on M&A as a key pillar in value creation, thereby increasing its reliance on capital markets to finance returns. Over the next decade, higher interest rates will constrain access to capital for private equity owned businesses, lowering the attractiveness of debt funded M&A to generate equity returns. The period of zero interest rates the United States entered in 2008 created a unique market opportunity to accumulate low cost acquisitions entirely funded with debt, generating substantial equity returns. Market participants competed away excess returns in this investment strategy by bidding up the cost of private equity platforms and tuck-in acquisition targets, creating a PE industry with significantly higher capital intensity than existed before. Higher interest rates will limit the availability of capital — both debt and equity — creating a significant change in how business owners will create value prospectively. Over the next decade, companies that efficiently create their own capital to finance their growth strategies will prevail. This article will explore the impact of high capital costs on businesses broadly, as well as the private equity industry’s favorite investment thesis specifically — roll ups.

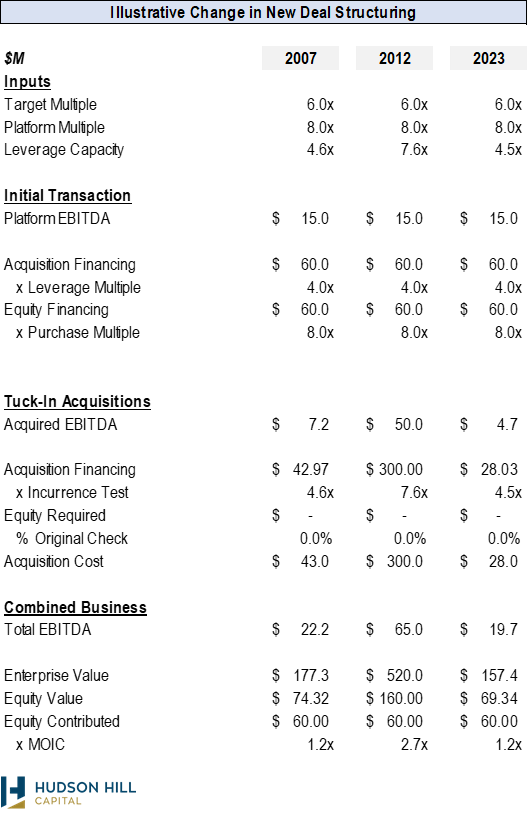

The recent fifteen year bull market in private equity created significant competition for private assets, driving up prices and therefore the amount of capital required to generate the same amount of return. In the table below, we compare the same, illustrative business acquired by a private equity firm in 2010 and 2022. Over this time, the cost of the initial platform rose to 11.9x EBITDA, up from 7.5x EBITDA. As a result of these higher prices, companies growing at the same rate — 10% — must therefore complete significantly more M&A to earn a 3.0x multiple of invested capital (MOIC) given M&A represents the only alternative to organic growth to create equity value. In 2010, a company growing EBITDA by 10% annually, would need to complete $26 million of “add-on” M&A to generate a 3.0x MOIC return. By 2022, entry multiples rose nearly 60%, requiring this same $15m EBITDA PE-backed company to complete $280 million of M&A to generate a 3.0x MOIC return (or 11x as much M&A). This means the average capital intensity (initial debt and equity, plus any acquisition capital) of investing in the same business for private equity firms increased by 3.2x from 2010 to 2022.

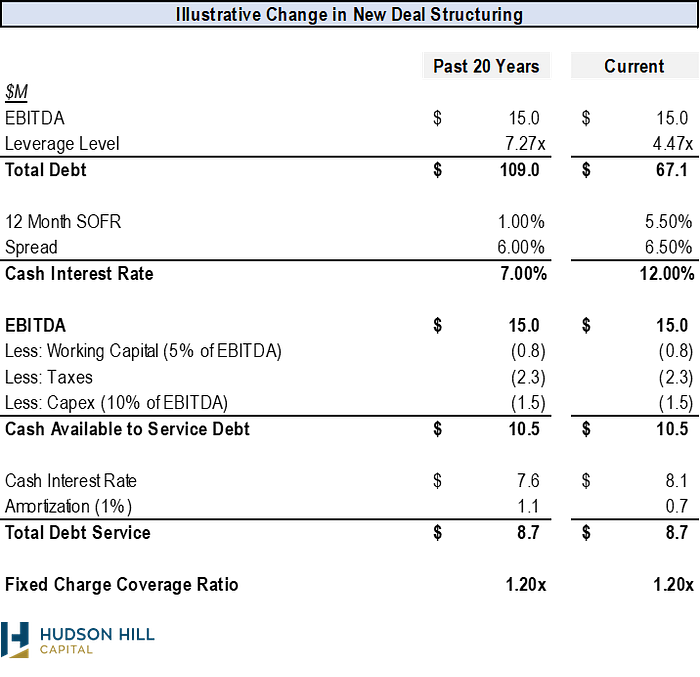

The capital intensity of the PE industry in 2022 came out of highly rational actions from sponsors. Returns to “add-on” M&A were incredibly attractive during the early 2010s, as a result of interest rate declines after the Financial Crisis. As you can see in the table below, interest rates move inversely to leverage capacity of companies. Interest rate declines in 2008 created significantly more leverage capacity for private equity-backed companies.

Private equity firms rationally utilized the nearly 100% increase in leverage capacity to acquire smaller companies with debt, creating significant equity returns in the process. In the below table, we illustrate the impact of the rapid decline in interest rates on the average PE-backed investment. In 2007, a PE-backed company could only acquire ~$7 million of EBITDA without requiring additional equity or organic growth. By 2012, a PE-backed company could acquire an infinite amount of EBITDA without additional equity by utilizing leverage capacity created by zero interest rates. As a result, equity returns of PE-backed companies became governed by the amount of M&A completed in an ownership period and nothing else. This dynamic created an immense opportunity for thousands of rational PE-backed companies to grow through M&A, which required significant capital that cost equity owners virtually nothing. The ability to create uncapped equity returns through very low-cost debt financing ended in 2022 as interest rates rose to levels seen before the most recent PE bull market (highlighted in the table below).

The individual rationality of PE sponsors created system-wide irrationality, as the prices of PE platforms rose every year in this bull market, creating a need for more and more “add-on” M&A to generate returns.

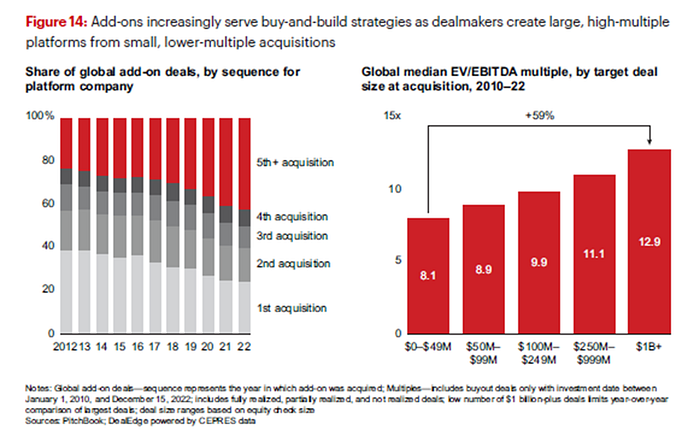

In the charts below, Bain’s most recent PE Report highlights the increasing reliance on M&A to create value for PE investments.

Prospectively, this capital-intensive approach to value creation will struggle. The table below illustrates the impact of higher interest rates on capital structures. Over the past fifteen years, companies could support leverage facilities of 7x+, driven by very low interest rates. By the end of 2023, companies will be able to support leverage facilities of 4.5x. The 40% reduction in debt capital available to PE-backed businesses will reduce the ability to grow through M&A.

Prospectively, companies need to generate their own capital to grow. Companies that rely heavily on external financing-based growth strategies will struggle with increased capital costs. For private equity it is important to understand that despite the enduring success of roll-ups over recent bull market, zero interest rates created this opportunity. The opportunity that existed in 2010 for PE-backed companies to aggregate an unlimited amount of earnings through very low cost debt financing ended in 2022. Numerous PE platforms established over the past five years with the goal of continuing this thesis will struggle to generate returns. The successful companies over the next decade will finance themselves through high returns on invested capital projects, eschewing expensive external financing markets.

At Hudson Hill, we feel we positioned our firm well to capitalize on this significant change in industry dynamics. We focus on building businesses in large addressable markets that possess significant organic growth opportunities. We provide guidance and support through our Strategic Advisory Board of seasoned industry executives that assist our companies from the board of directors on all matters of strategy and operations. We complement this board level engagement with our Portfolio Transformation Team of functional experts across all aspects of business building — from business intelligence to human capital, to go-to-market, and digital transformation. The PTG seeks to assist founder-led businesses compress the time it takes to transform their businesses into institutionally backed companies better positioned to capture their market opportunity. While the significant change in interest rates will profoundly impact the private equity industry, we feel we positioned Hudson Hill and its portfolio companies well to take advantage of the opportunity it creates.